Welcome to the second part of our series on biodiversity and the TNFD. To get caught up—and learn more about why biodiversity has become such a pivotal topic in the ESG space—check out Getting Started with Biodiversity and the Taskforce on Nature-Related Financial Disclosures.

How many of us return from each holiday period still dreaming of the time we were lucky enough to spend outside—by the beach with a book in hand, out for walks in nature, playing water or snow sports, or simply spending time with ourselves, friends, and family enjoying the fresh air and landscapes around us? How many of us have a hard time adjusting to indoor, desk-bound corporate work and begin counting down the hours to get out for a breath of fresh air?

What we’re all craving is that serotonin-boosting, energizing feeling we get from being amongst nature. Time spent outdoors is both made possible and enhanced by the quality of ecosystem services in those environments—those essential benefits that a functioning ecosystem provides to humans. These services include clean air and water, regulation of a stable and temperate climate, and those behind-the-scenes processes such as pollination from bees and bats which makes things like food production possible.

Perhaps it seems obvious that nature’s services allow the natural world to survive—and that humans benefit from this. But when sitting at our desks or in meeting rooms making business decisions for the years to come, we are rarely drawing the connection between nature’s essential services and the survival of our businesses in the long term.

This is where the TNFD has stepped in

The Taskforce on Nature-Related Financial Disclosures (TNFD) is a market-led and science-based initiative made up of forty individual taskforce members from a range of financial institutions, corporates, and market service providers around the world. The TNFD was launched in 2021 to design a framework for businesses to begin reporting on nature-related issues such as their impacts, dependencies, risks and opportunities as they relate to nature (see our last blog in this series for a breakdown of what these terms mean).

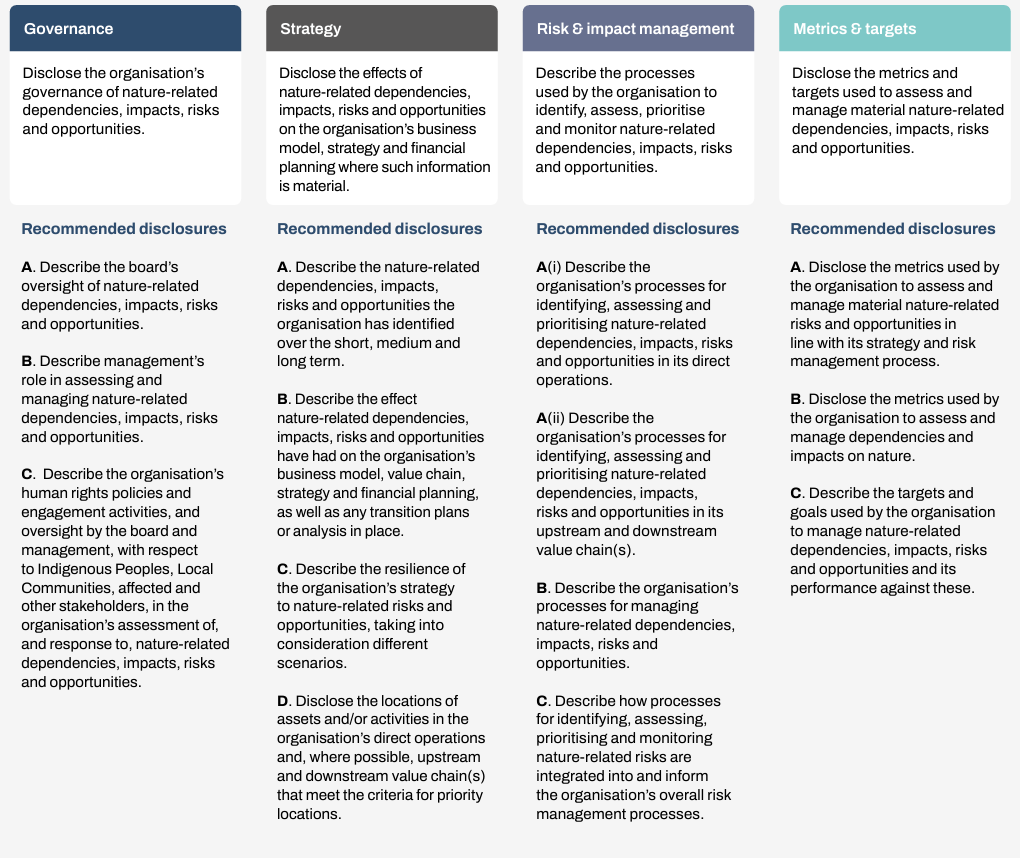

In other words, it was the TNFD’s mission to provide businesses with the tools to start understanding and assessing how intrinsic nature is to their survival (and success). In September 2023, the TNFD delivered on the first milestone of this mission by releasing its Recommendations which include fourteen recommended disclosures, as well as a suite of Guidance Documents to support their implementation.

These disclosures build upon the TCFD, or Taskforce on Climate-Related Financial Disclosures, by covering disclosures on organizations’ nature-related:

- Governance

- Strategy

- Risk & Impact Management

- Metrics & Targets

Similarly to TCFD, the TNFD has started as a voluntary framework which businesses can choose to report against alongside annual financial reporting. That said, it’s anticipated that many jurisdictions around the world will begin to incorporate the TNFD’s recommended disclosures into local regulatory reporting schemes or potentially mandate TNFD reporting, as we saw with the TCFD.

Multiple existing and emerging schemes have been increasing nature-related reporting requirements of late, such as the Global Reporting Initiative (GRI), S&P Global’s Corporate Sustainability Assessment (CSA), EcoVadis, and CDP, which will begin to align its questionnaire with the TNFD this year. The European Sustainability Reporting Standards (ESRS) are the first to mandate nature-related reporting for companies with operations in the EU, with the standards being fully aligned to the TNFD’s fourteen recommended disclosures. These developments all come under the backdrop of the Kunming-Montreal Global Biodiversity Framework which was adopted at COP15 in Montreal 2022, aiming to halt and reverse biodiversity loss by 2030, with twenty-three targets supporting this overall goal.

Let’s jump into the ins and outs of the TNFD’s framework itself, focusing on the general requirements, comparing the recommended disclosures against the TCFD framework, and discussing why every organization should be paying attention.

TNFD General Requirements

Like any reporting framework, the TNFD has established its “rulebook” to help guide reporting entities as they approach the identification, assessment, and reporting of nature-related issues. While it may be tempting to skip past this “dry” section of the article or TNFD Guidance, it’s quite crucial that businesses understand the context within which they’re being asked to report on these topics.

TNFD’s general requirements set users up for success from the get-go by outlining how to approach various aspects of reporting and ensure consistency with other reporting entities.

As a brief summary*, the six requirements are:

1. Application of materiality

Apply the definition of materiality provided by your jurisdiction’s regulatory authority for disclosing nature-related dependencies, impacts, risks, and opportunities.

In the absence of such a definition:

- The ISSB’s approach to materiality is recommended (financial materiality).

- You may choose to employ a double materiality approach (financial and impact materiality).

2. Scope of disclosures

Describe the scope of TNFD-related assessments and reporting in detail, including:

- The boundaries of assessments and disclosures, such as which activities and assets across the entire value chain are included or excluded.

- The relevant contribution of each activity or asset that was included or excluded (e.g., the % a facility contributes to total revenue).

- The process used to determine which elements were within scope.

Also, describe:

- Which of TNFD’s 14 recommended disclosures you are disclosing.

- How the scope of disclosure is expected to change in future, including if material risks, dependencies, and impacts aligned to Target 15** of the Global Biodiversity Framework will be disclosed.

3. Location of nature-related issues

Dependencies and impacts on nature are often location- or ecosystem-specific. Therefore, it is best to consider geographic location when assessing nature-related issues, and to disaggregate information, where possible.

Consider:

- Issues covering specific individual locations or ecosystems.

- Issues covering multiple locations or ecosystems.

- Direct operations, upstream, and downstream value chain issues.

4. Integration with other sustainability-related disclosures

Integrate nature-related disclosures with other business and sustainability-related disclosures when possible.

Identify the relationship between your organization’s climate- and nature-related targets and actions. Can you pinpoint any alignment, synergies, or trade-offs?

5. Time horizons considered

Describe what are considered as short-, medium-, and long-term time horizons.

Take into account that nature-related risks and opportunities may take some time to manifest.

6. Engagement of Indigenous Peoples, local communities, and affected stakeholders

Describe your organization’s process for engaging Indigenous Peoples, local communities, and affected stakeholders in the identification and assessment of nature-related issues. What are these stakeholders’ concerns and priorities, and how has your organization taken these into account?

Consider:

- Dependencies, impacts, risks, and opportunities.

- Direct operations, upstream, and downstream value chain issues.

Comparing the TCFD and TNFD

After more than a year of market consultation and pilot testing, the TNFD finalized fourteen recommended disclosures for framework users. As described earlier, these disclosures build upon the TCFD’s eleven recommendations, with the focus expanding from climate-related risks and opportunities only, to nature-related dependencies, impacts, risks, and opportunities.

Dependencies—those aspects of nature and ecosystem services a business relies on to function—and impacts—the positive or negative effects a business has on the state of nature—are crucial inclusions to the TNFD’s framework. These elements address the heightened complexity of assessing a company’s relationship with nature, as opposed to climate.

Recommendations of the Taskforce for Nature-related Financial Disclosures, September 2023, p. 47

New disclosures

When compared to the TCFD framework, the TNFD framework includes two important additions: reporting related to human rights and locations of operation.

Human rights

Disclosure C under Governance asks companies to disclose information about their consideration of Indigenous Peoples, Local Communities, affected and other stakeholders in their assessments of and response to nature related-issues. What does this mean in practice?

As part of a company’s TNFD reporting, they are expected to explain how their policies, commitments, engagement activities, and oversight of these elements by governing bodies work in practice to consider the significance of Indigenous Peoples and local communities in their real or potential nature-related impacts, dependencies, risks, and opportunities – as well as how to best manage them. This could play out in a variety of ways, but examples of questions that reporting companies might want to consider include:

- How do your human rights-related policies and commitments work to reduce your negative impacts and increase your positive impacts on local communities or Indigenous groups?

- How do your engagement activities demonstrate that Indigenous Peoples’ knowledge of and activities to protect and restore nature are something you depend on for success?

- What risks might you be exposed to if Indigenous Peoples’ or local communities’ human rights are infringed upon by your activities as they relate to nature (e.g., contamination of water sources, removal of native vegetation, damage of sacred sites)?

- How might positive engagement activities with local communities and Indigenous Peoples create opportunities both for you and your stakeholders as they relate to nature (e.g., partnerships for nature-based solutions***, job opportunities, ecosystem conservation)?

Under this TNFD recommended disclosure, companies are required to specifically refer to their commitments under international frameworks such as the UN Guiding Principles on Business and Human Rights, the UN Declaration on the Rights of Indigenous Peoples, and the UN General Assembly Resolution 76/300 on rights to a healthy environment, among others. The concept of Free, Prior, and Informed Consent (FPIC) is prevalent here, which refers to the need to consult Indigenous Peoples on issues that affect them, particularly with regard to projects occurring on their land. As outlined in the UN Declaration on the Rights of Indigenous Peoples, FPIC requires that Indigenous people provide consent which is free from coercion, occurs prior to the activities being undertaken, and is well-informed.

The TNFD encourages companies to develop a deeper understanding of the symbiotic relationship between the wellbeing of nature and the wellbeing of Indigenous Peoples and local communities, taking this into account when making business decisions related to nature. CDP’s Forests questionnaire has incorporated FPIC for many years, asking how organizations promote the principle in areas such as organizational policies, public commitments, supply chain engagement, and executive remuneration.

Locations of operation

Another key distinguisher between TCFD and TNFD is the addition of Disclosure D under Strategy, which asks companies to disclose locations in its direct operations (and upstream and downstream value chains where possible) in “priority locations.”

Priority locations can be categorized in two ways (though there is likely to be crossover):

Material locations: Locations where “an organization has identified material nature-related dependencies, impacts, risks, and opportunities in its direct operations and value chain.”

Sensitive locations: Locations where “the assets and/or activities in its direct operations and value chain interface with nature” in:

- Areas important for biodiversity

- Areas of high ecosystem integrity

- Areas of rapid decline in ecosystem integrity

- Areas of high physical water risks

- Areas of importance for ecosystem service provision, including benefits to Indigenous Peoples, local communities, and stakeholders (TNFD Recommendations)

Why should companies specify priority locations? The assessment of nature and biodiversity is extremely location-specific due to the interplay of different species, biomes, weather patterns, and other biological factors relevant to an area. To effectively understand an organization’s nature-related impacts, dependencies, risks, and opportunities, it’s essential that the locations in which it operates are assessed to determine if they may be “material” or “sensitive” locations. We’ll go into more detail on how these assessments can be undertaken later in this blog series.

Risks and impacts across the value chain

The final differentiator between TCFD and TNFD recommended disclosures lies in the Risk and Impact Management category, where organizations are asked to disclose information on their processes for identifying, assessing, and prioritizing nature-related issues that occur in their direct operations (disclosure A (i)) and their upstream and downstream value chains (disclosure A (ii)). This takes a more detailed approach than TCFD, requiring organizations to have a specific handle on the different mechanisms in place to manage nature-related issues across its value chain.

The interdependence of climate and nature reporting

While there are some key differences between the frameworks, TNFD’s fourteen disclosures were designed to complement the TCFD’s disclosures, with the intention that companies will start to report their nature-related information alongside that of climate, since the two topics are inextricably linked.

It is widely acknowledged that global climate goals (such as reaching net zero emissions by 2050) cannot be met without meeting similar targets for the protection and restoration of nature (such as the 2030 goals established under the Kunming-Montreal Global Biodiversity Framework), and vice versa. Since the business community plays such a critical role in achieving these targets, organizations around the world are increasingly expected to assess and report on nature to the same extent as, and in conjunction with, climate change.

Although the TCFD has now been absorbed into the International Sustainability Standards Board’s (ISSB) reporting standards, TNFD disclosures remain separate and are to be reported alongside their counterpart climate information, such as how climate- and nature-related issues are governed, how climate- and nature-related risks are identified and managed, and so on. Companies who can effectively make these connections—which are present across every sector and region of operation to varying degrees—will be best placed to holistically manage and report on some of the largest ESG challenges the world will face in coming years.

Why every organization should prioritize TNFD reporting

So, who does all this information really apply to? Does an I.T. services company need to pay as much attention to the TNFD as a mining company? What about companies operating in jurisdictions or sectors with stronger environmental and social laws in place—should they be taking as much notice as companies whose activities cover supply chains with traditionally less regulation?

Of course, the extent of the impacts, dependencies, risks, and opportunities an organization has on nature will vary significantly based on the context of its operations. However, there is a common misconception that companies that don’t directly interact with nature for revenue generation are exempt from nature-related issues. The work of the TNFD to date proves this idea wrong by exposing the huge variety of ways nature is relevant to all businesses and the traditional measure of business success: the bottom line.

At the simplest level, business activities rely upon people, places, and resources to function. Without functioning ecosystems—which produce and reproduce natural elements and services—people, places, and resources cannot exist. As nature and biodiversity have become increasingly under threat from large-scale human activities, it is crucial for every company to recognize its contribution—however small—to the problem, and the ways it could be affected by future risk and opportunities related to nature.

ADEC ESG works with organizations around the world to help improve their ESG disclosure and reporting programs and achieve their sustainability goals. To chat with us about how we can support your organization’s nature-related programs, goals, or disclosures—including services such as TNFD Feasibility Assessments or Gap Analyses—contact our team today.

*See pages 43-46 of TNFD’s Recommendations paper for more information on how the general requirements should be applied

**Target 15 of the Global Biodiversity Framework: Businesses Assess, Disclose and Reduce Biodiversity-Related Risks and Negative Impacts

***Nature-based solutions refer to actions that protect, manage, or restore ecosystems in ways that provide benefits to both the ecosystems and affected communities at the same time.